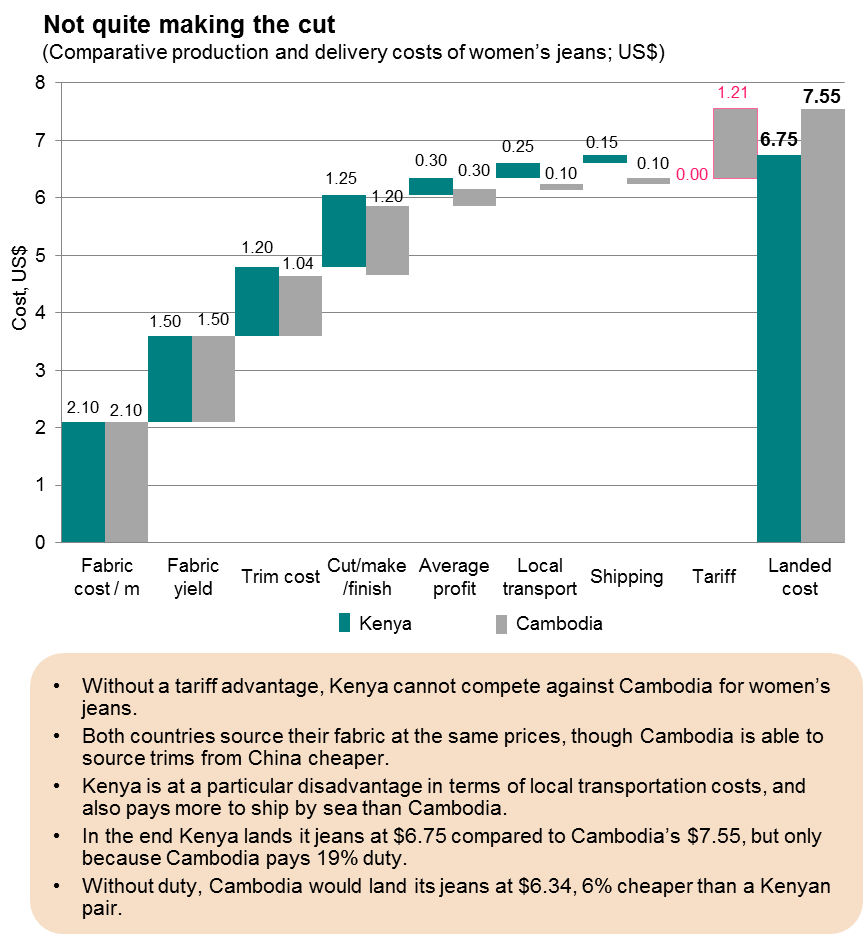

Kenya’s

textile and apparel's industry struggles to remain competitive against its global rivals.

This became clear when its sales dropped as a result of the increased opening

of the US market to China’s exports in 2005. Since then the Chinese threat has

since been held at bay with imposition of restrictions, but should these not be

renewed, the results will be very harmful to Kenya’s industry.

However,

China is not the sole threat. India, Bangladesh and Cambodia all have strong

textile and apparel sectors. While India’s sector may still be restricted in

the same way as China’s, it is increasingly difficult for US policy-makers to

justify trade advantages offered to African

countries over Bangladesh and Cambodia, which are equally poor.

As

far back as 2007, The

Economist magazine wrote about Africa's AGOA-fueled apparel industry:

… the future is uncertain.

American, European and South African quotas on Chinese exports are likely to be

abolished within the next couple of years. The World Trade Organisation has also decided that rich

countries should extend preferential access to all poor countries, not just

African ones…

Time

is running out on AGOA,

not so much in terms of its formal expiry in 2015 (AGOA will likely be extended

beyond 2015, as has happened before), but more in terms of whether meaningful

advantages can continuously be offered to African states.

Therefore,

Kenya’s textile and apparel exporters will need to develop a business advantage

over their competition based on firm-level advantages, rather than advantages

offered by US trade policy.